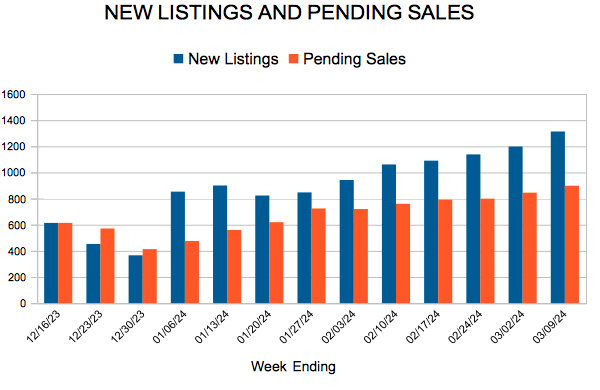

New Listings and Pending Sales

For Week Ending March 9, 2024

For Week Ending March 9, 2024

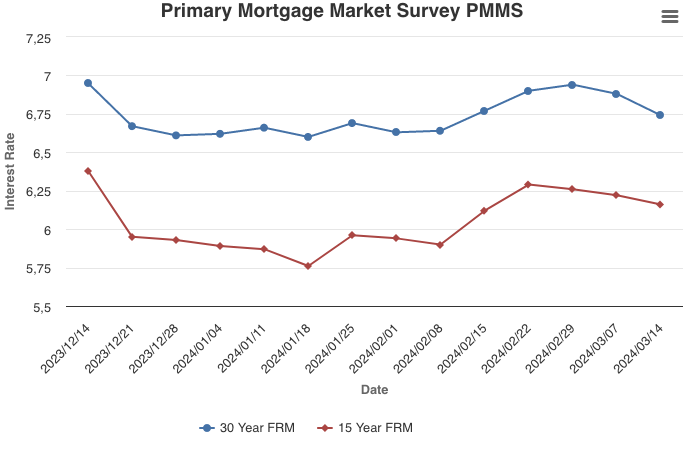

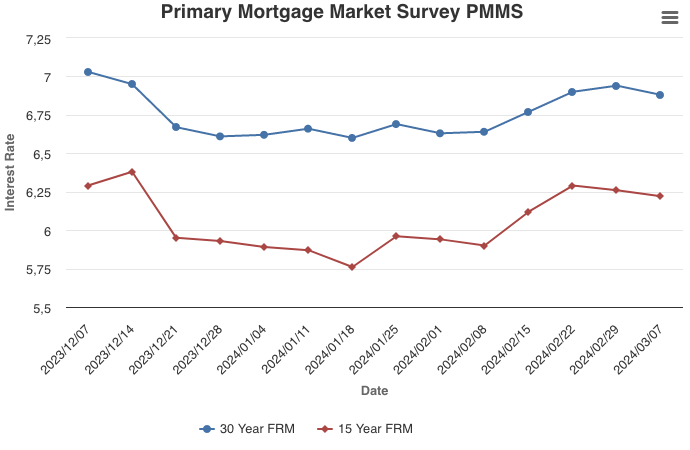

Mortgage rates fell for the first time in five weeks, as the average 30-year fixed rate mortgage slid 0.06 percentage points to 6.88% the week ending March 7, 2024, according to Freddie Mac. The decline in rates helped mortgage applications increase 7.1% on a seasonally adjusted basis from the previous week, according to the Mortgage Bankers Association, while applications to purchase a home were up 5% from the previous week.

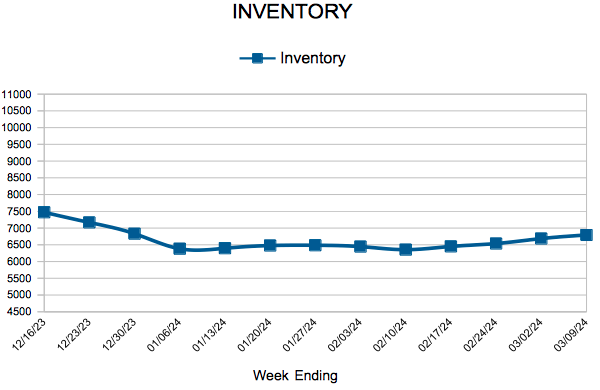

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING MARCH 9:

FOR THE MONTH OF FEBRUARY:

All comparisons are to 2023

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

March 14, 2024

The 30-year fixed-rate mortgage decreased again this week, with declines totaling almost a quarter of a percent in two weeks’ time. Despite the recent dip, mortgage rates remain high as the market contends with the pressure of sticky inflation. In this environment, there is a good possibility that rates will stay higher for a longer period of time.

Information provided by Freddie Mac.

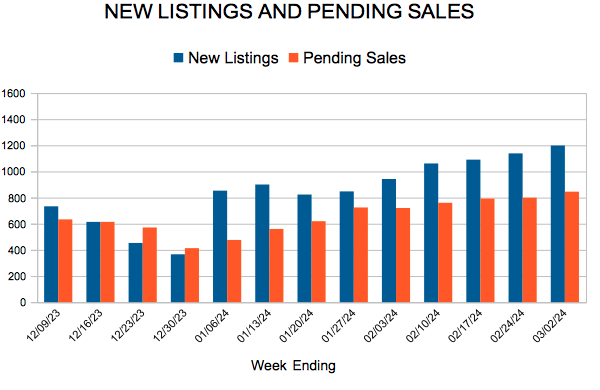

For Week Ending March 2, 2024

For Week Ending March 2, 2024

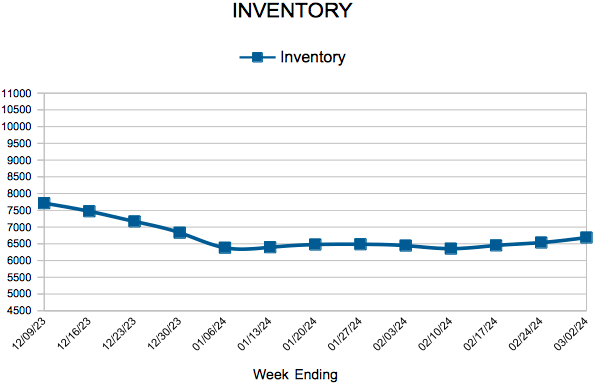

The limited supply of existing-home inventory nationwide continues to benefit the new-home market, with applications for new home purchases up 38% month-over-month and 19.1% year-over-year in January, according to the Mortgage Bankers Association Builder Application Survey. The latest reading marks the 12th consecutive annual increase and is the strongest non-seasonally adjusted reading for the month in the survey’s history.

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING MARCH 2:

FOR THE MONTH OF JANUARY:

All comparisons are to 2023

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

March 7, 2024

Evidence that purchase demand remains sensitive to interest rate changes was on display this week, as applications rose for the first time in six weeks in response to lower rates. Mortgage rates continue to be one of the biggest hurdles for potential homebuyers looking to enter the market. It’s important to remember that rates can vary widely between mortgage lenders so shopping around is essential.

Information provided by Freddie Mac.

In the ever-evolving realm of real estate, the current landscape is nothing short of dynamic. A whirlwind of factors has shaped the market, creating a ripe environment for homeowners to seize exciting opportunities. Let’s take a captivating journey through the elements that have transformed the real estate arena.

Picture this: near-record low interest rates beckoning aspiring homeowners into a world of affordability. The financial stars have aligned, making home financing more accessible than ever. It’s a golden era for those looking to step onto the property ladder or make a savvy move in the market.

However, it’s not all smooth sailing. A constant drumbeat in the real estate symphony is the low inventory blues. The scarcity of available homes has become a defining trend, turning the home-buying experience into a competitive sport. Buyers, armed with determination, are battling it out for their dream dwellings in a market where supply is the hottest commodity.

Enter the era of high demand—a confluence of low interest rates and a collective yearning for more comfortable living spaces during lockdowns. The result? A surge in buyer demand that has sent shockwaves through the real estate cosmos. It’s a seller’s market, and homes are commanding attention like never before.

The interplay of these dynamics has given rise to a noteworthy consequence: a significant escalation in home values. Chances are, your property has felt the impact of this upward trend. The question now is, how can you leverage this to your advantage?

Did you put down less than 20% when you purchased your home? Now might be the opportune moment to bid farewell to Private Mortgage Insurance (PMI). The surge in your home’s value could empower you to eliminate PMI, paving the way for lower monthly payments. Curious if this applies to you? A comprehensive market analysis holds the answers.

Eyeing a new abode? Your increased equity is your golden ticket. Let’s embark on a conversation about your equity position and explore what the exciting journey of purchasing a new home looks like for you.

Life is a series of changes, and so are housing needs. Whether you’re ready to upsize, downsize, or simply crave something new, I’m here to guide you through the process. Let’s align your dreams with your home’s value and make your housing aspirations a reality.

In a real estate landscape that’s alive with possibilities, it’s time to turn the page and explore the exciting chapters waiting for you. Let’s navigate the thriving market together and unlock the full potential of your real estate journey

Home loans that conform to the Fannie Mae and Freddie Mac guidelines tend to have better terms than non-conforming loans. That’s why it’s good news that the Federal Housing Finance Agency (FHFA) recently announced that the conforming loan limits have increased to $766,550 for 2024. This is a $40,350 increase from the $726,200 loan limits of 2023. In some higher-cost areas, the loan limits could be as high as $1,149,825, which is a $60,525 increase from the $1,089,300 high-cost loan limits of 2023. Click here to view a map of all the loan limits across the US. Here are two ways to benefit from this increase:

It may make sense for you to consider a new home purchase using the higher loan amounts. This may be the perfect time for you to lock in your interest rate before interest rates move higher.

It may be worth it to consider a home loan refinance if:

Credit/Original Source: CertfiedRealEstateAdvisor

Greet me and meet me on social media. You can follow my new listings and changes in the marketplace on any of the following.

Follow me.