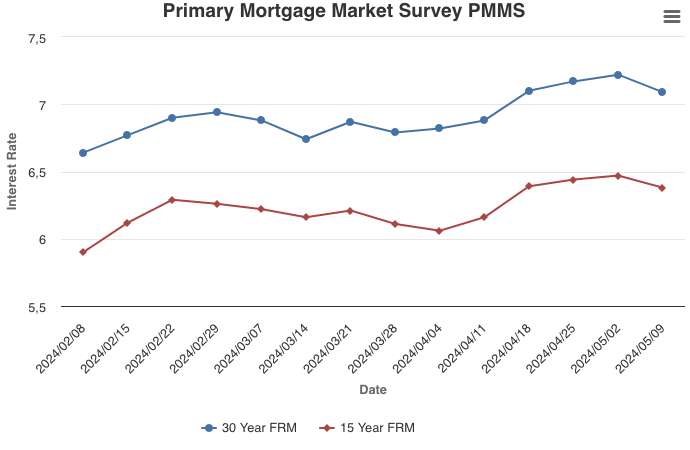

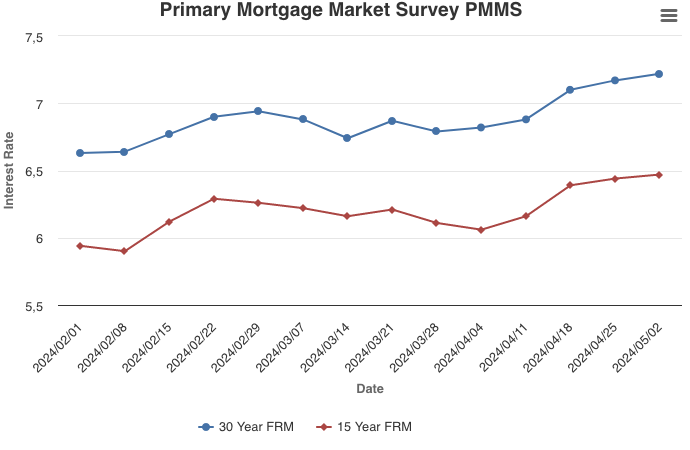

For Week Ending May 4, 2024

For Week Ending May 4, 2024

The best time to sell a home is in the first half of the year, according to a new report from ATTOM. An analysis of more than 59 million home sales from 2011 to 2023 showed that the months of May, February, and April offer the highest seller premiums, at 13.1%, 12.8%, and 12.5% above market value, respectively. The best day of the year to sell a home? May 27, with a seller premium of 16.2%, according to the report.

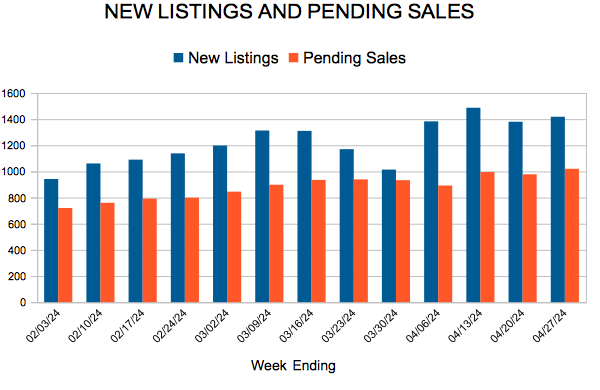

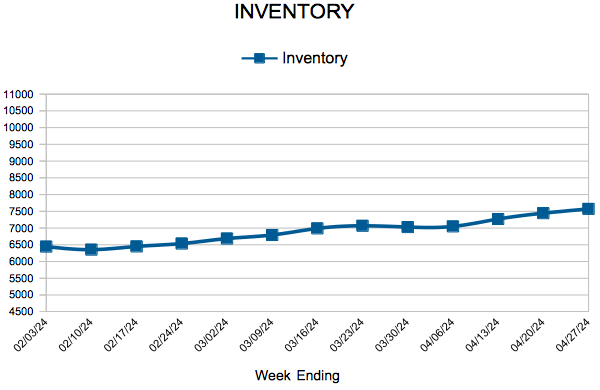

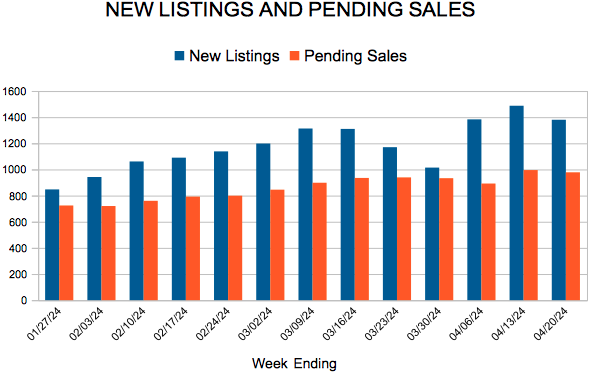

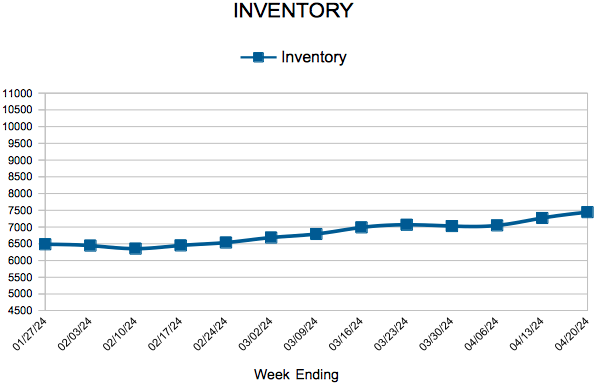

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING MAY 4:

- New Listings increased 0.2% to 1,591

- Pending Sales decreased 2.8% to 1,082

- Inventory increased 14.7% to 7,750

FOR THE MONTH OF MARCH:

- Median Sales Price increased 2.8% to $366,000

- Days on Market decreased 6.9% to 54

- Percent of Original List Price Received increased 0.2% to 98.8%

- Months Supply of Homes For Sale increased 26.7% to 1.9

All comparisons are to 2023

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.