PHOTO: EMILY FOLLOWILL; DESIGN BY WYETH RAY INTERIORS

Expert advice to thwart uncomfy sofas and buyer’s remorse.

Much to the consternation of our wallets (and our better judgment), a little impulse shopping is hardly the end of the world. That is, unless you’ve gone and made a major, spontaneous purchase. Then, you just might find yourself facing an over-extended budget and buyer’s regret.

Furniture is one thing that should never be bought on a whim. This is one impromptu purchase that is far too expensive, heavy, and burdensome to replace if you decide to return it as quickly as you bought it.

Instead, interior designers recommend taking your time when shopping for furniture, and putting some serious thought and planning in before making any decisions. For example, designer Caroline Agee advises furniture shoppers to consider functionality, style, durability, and cohesiveness before taking anything home with them.

When shopping for new furniture, keep notes with you about ideal dimensions and bring fabric swatches with you while you shop. Anything you can do to feel more confident in your choice will lead to less buyers remorse.

To make the smartest furniture buying decisions possible, we’ve compiled a list of mistakes to avoid. Interior designers say that ignoring these oversights may lead to disappointing furniture that’s improperly scaled, low quality, or not meant for the long haul.

Buying First, Planning Later

Before you even begin browsing, a planning stage is essential, designers reveal. Shopping unprepared might just be the biggest furniture woe yet.

“Purchasing furniture isn’t like purchasing artwork,” says Ray. “With art, you can almost always find a home for it. Artwork doesn’t need to necessarily work with anything else in the space. With furniture, it needs to be the right size, color scheme, and style to fit in with your space.”

Agee agrees, sharing her strategy to bypass this miscalculation: “I always determine what dimensions would work best before I begin looking for a piece of furniture,” she says. “It’s best to have a furniture layout for a space so you have a long-term plan. Having a plan not only helps determine what dimensions will work best, but also helps to coordinate the style, fabric, and finishes of multiple pieces. It also helps to avoid ending up with pieces that don’t end up working.”

Overlooking Function

Considering function before shopping is top priority, designers say. With some foresight, you’ll surely save yourself lots of time shopping around and ultimately settle on a more fitting piece of furniture.

“Think about functionality for a space,” says Agee. “For instance, you may have room for a console table, a chest with drawers, or a cabinet with doors. Having an idea of what will function best helps you spend less time searching for the right piece.”

This rule applies to both choosing what kind of furniture you’re on the prowl for, as well as critical details. Agee also says that one common mistake she sees furniture shoppers make is not putting enough thought into what kind of fabric will best suit their functional needs for an upholstered piece. Consider your durability needs, she says, and interior designer Sarah Brannon recommends that shoppers consider whether or not they wish to choose a performance fabric.

Living Solely In The Moment

When shopping for furniture, think long-term. Interior designers agree that considering longevity is critical—both from a quality and design perspective. Ray recommends avoiding short-lived trends and asking yourself the questions: “Will I love this in 5 years? 10 years?”

At times, thinking long-term might even mean making sacrifices in the short term. These days, furniture can take what feels like ages to arrive, but Agee reassures that timeless, quality furniture will be worth the wait.

“I think people often want what’s available the soonest or they want to save money by buying a less expensive piece of furniture,” she says. “The best way to be happy with furniture for a long time is by carefully weighing the options and being okay with spending a little bit more or waiting slightly longer for it to arrive. Of course, if you spot a one-of-a-kind piece that you love, you should go for it!”

Buying To Fill A Gap

Like decor, furniture shouldn’t be purchased only for the sake of closing a gap. Just because you’re in the market for a new coffee table, doesn’t mean that you should settle for the first one you see.

“Furniture shouldn’t be purchased simply because you have a hole to fill,” says Ray. “It should be something that caught your eye compared to all of the other options. Something that drew you in.”

Taking Furniture At Face Value

Looks aren’t everything. Like for people, beauty has to come from the inside. In fact, if something must slip through the cracks, it should be design over quality. While falling for a short-lived furniture trend isn’t advisable, it’s much easier to fix the look of a piece than its foundation.

“I have consigned pieces that no longer work with my aesthetic,” Agee admits to her own past furniture mistakes. “Quality pieces can be transformed with paint, a new finish, or new hardware too.”

To avoid such missteps, Ray recommends researching a piece rather than simply being satisfied with the look of it online or in a showroom. Once you find a piece of furniture you’re interested in, take a step back and do your due diligence to make sure it’s right for you.

“Do your research on the quality of the piece,” Ray advises. “What materials is the piece made from, for instance is it real wood, and what kind of cushion content does it contain? Even if something is inexpensive, you’re throwing away money if it isn’t going to last you but a year or two.”

:max_bytes(150000):strip_icc():format(webp)/coastal-living-room-2444801-25513-1-0c7c160af0874e0495bb84b6f706d6c9.jpg)

Bony Upholstery

Having selected many pieces of furniture in her days as a designer, Ray reveals that there’s a sure-fire way to tell if a piece of upholstery is quality enough to consider buying.

“If you push on the arm or back of upholstery and can feel the wood through the fabric, it’s going to be a no,” she says. “Look for thicker upholstery with plenty of cushion. Remember, when viewing furniture in a store or showroom, you are seeing the best that a piece of furniture is going to look, so you need to feel it’s of good quality.”

When you sit and sample on a showroom piece, if it demonstrates this red flag, then the furniture is immediately out of the running, Ray says—not even worth moving on to the research phase.

One-Stop-Shopping

“Do not one-stop-shop for your room,” Brannon pleads. “Mix it up from various places and select colors, patterns, and textures that are interesting!”

In addition to building a space that’s layered and appealing, considering multiple stores is a reliable way to avoid making an impulsive purchase. Agee recommends shopping around for the best piece to suit your needs, style, and budget before coming to any decisions.

“Once I have an idea of the style and dimensions of the piece I’m looking for, I like to look at multiple stores for similar pieces that I like,” she says. “Then I can compare them based on a number of criteria, like price, finish options, and lead time. Comparing multiple pieces helps me eliminate which ones aren’t my favorite. This helps me feel like I’m making the best decision and prevents buyer’s remorse.”

Pigeon-holing Pieces

When shopping for multiple pieces of furniture, another way to shop for furniture to build an interesting and layered space is to push the boundaries of design. Rather than feeling limited by a strict color palette, design style, or any other constraints (apart from space), creativity is encouraged.

“I love when various design styles are used cohesively in one space,” Agee says. “My favorite rooms incorporate old and new pieces in various finishes. It’s fun to mix a neoclassical antique with a mid-century modern piece, and sleek current upholstered pieces. Mixing styles and finishes helps a space feel collected and personal to the homeowner.”

Bad Bones

A reliable and beautiful piece of furniture that’s in it for the long haul begins with good bones. Cushions can be replaced, wood can be restrained, and fabric reupholstered, but if the foundation of a piece of furniture fails, you’ll be back at square one of the furniture shopping dilemma.

“It’s important to pick furniture pieces with good lines,” says Agee. “A new coat of paint or fabric can’t fix a bad silhouette. I look for silhouettes that are sleek and timeless.”

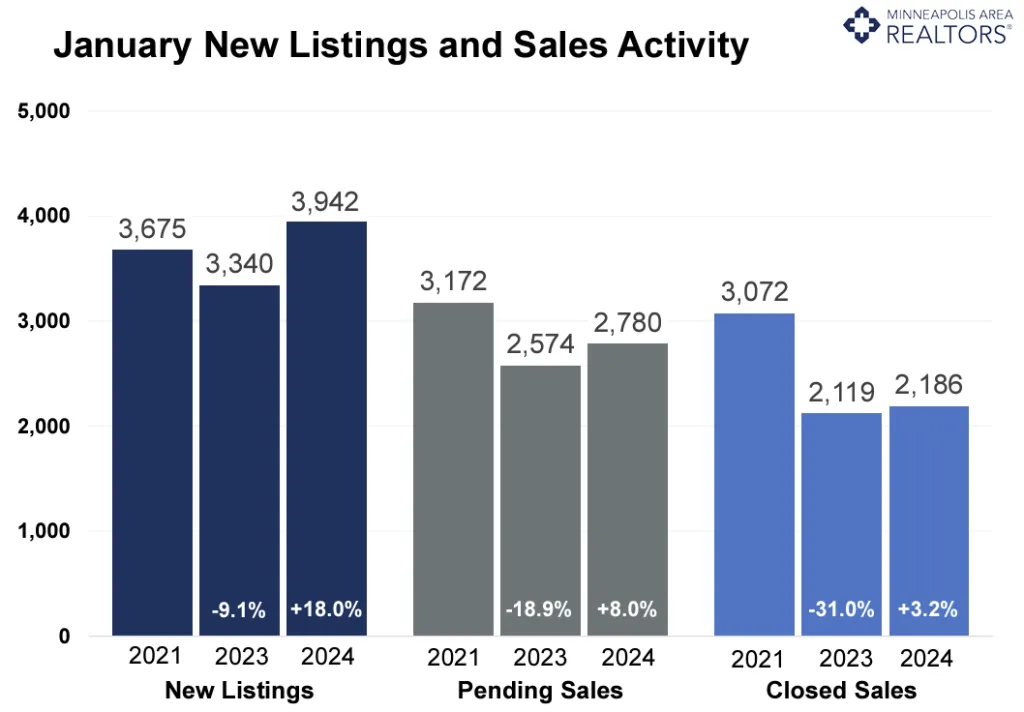

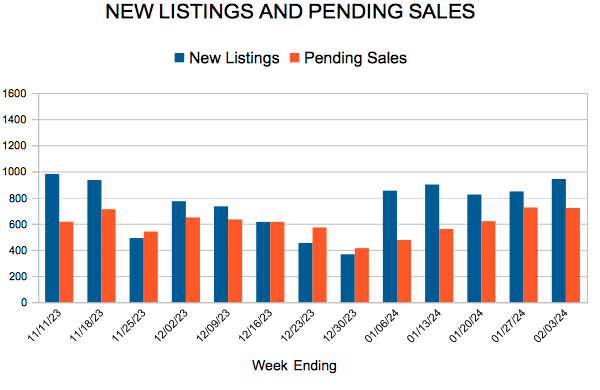

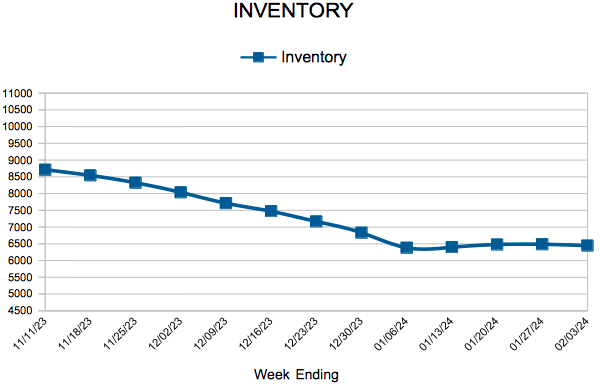

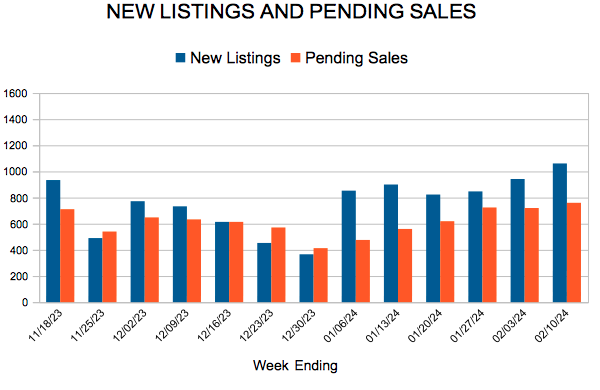

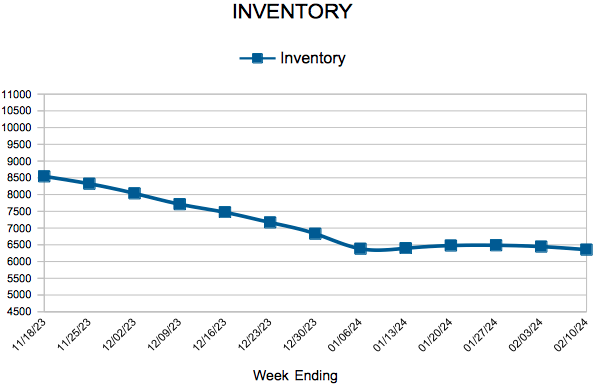

For Week Ending February 10, 2024

For Week Ending February 10, 2024